Over the past three years, real world tokenization has grown by nearly 20x in market cap and has now crossed $29 billion as per data from rwa.xyz. The scale of growth has drawn a formal response from the International Monetary Fund, a clear sign that tokenization is emerging as a real layer of financial infrastructure. This report highlights just how big this market has become and how investors are positioning during this shift, based on our latest newsletter poll.

What Are Tokenized Assets?

Simply put, tokenized assets are digital representations of real-world assets. This includes assets like real estate, government bonds, private credit, commodities and equities which are recorded and traded on a blockchain. Tokenized assets, as the name suggests, converts ownership rights into tokens which allows for fractional ownership, 24/7 trading, instantaneous settlements and the transparency that comes with being on the blockchain.

The main use case of tokenized assets is making traditionally inaccessible markets accessible. A retail investor who could never buy a stake in a U.S. Treasury funds or a commercial property can now do so via a tokenized product. An institution can use a tokenized bond as collateral in a DeFi protocol while still earning yield. These are real benefits that are live and being used more and more with each passing day.

How Large Has This Market Become?

In April 2023, the total RWA value was at around $1.4 billion. Fast forward three years and today that number has ballooned to over $29 billion with Standard Chartered projecting the market to reach $2 trillion by 2028. The real growth took place last year as the market grew from $5.79 billion at the start of the year to finishing the year at $21.39 billion.

Last year was particularly pivotal for a couple of reasons. Firstly, regulatory clarity in the U.S. (passing of the GENIUS Act and progress on the CLARITY Act) and Europe’s MiCA regime, reduced uncertainty around how tokenized assets would be classified, giving institutions the confidence to begin allocating.

At the same time, yield emerged as the defining use case. With interest rates elevated, tokenized U.S. Treasuries offered a compelling combination of familiar returns and on-chain utility, turning RWAs into productive, composable assets rather than passive holdings.

Finally, infrastructure caught up to ambition. Advances in custody, compliance layers, and on/off-ramps made tokenized products not just investable, but usable at scale, bridging the gap between traditional finance and on-chain markets.

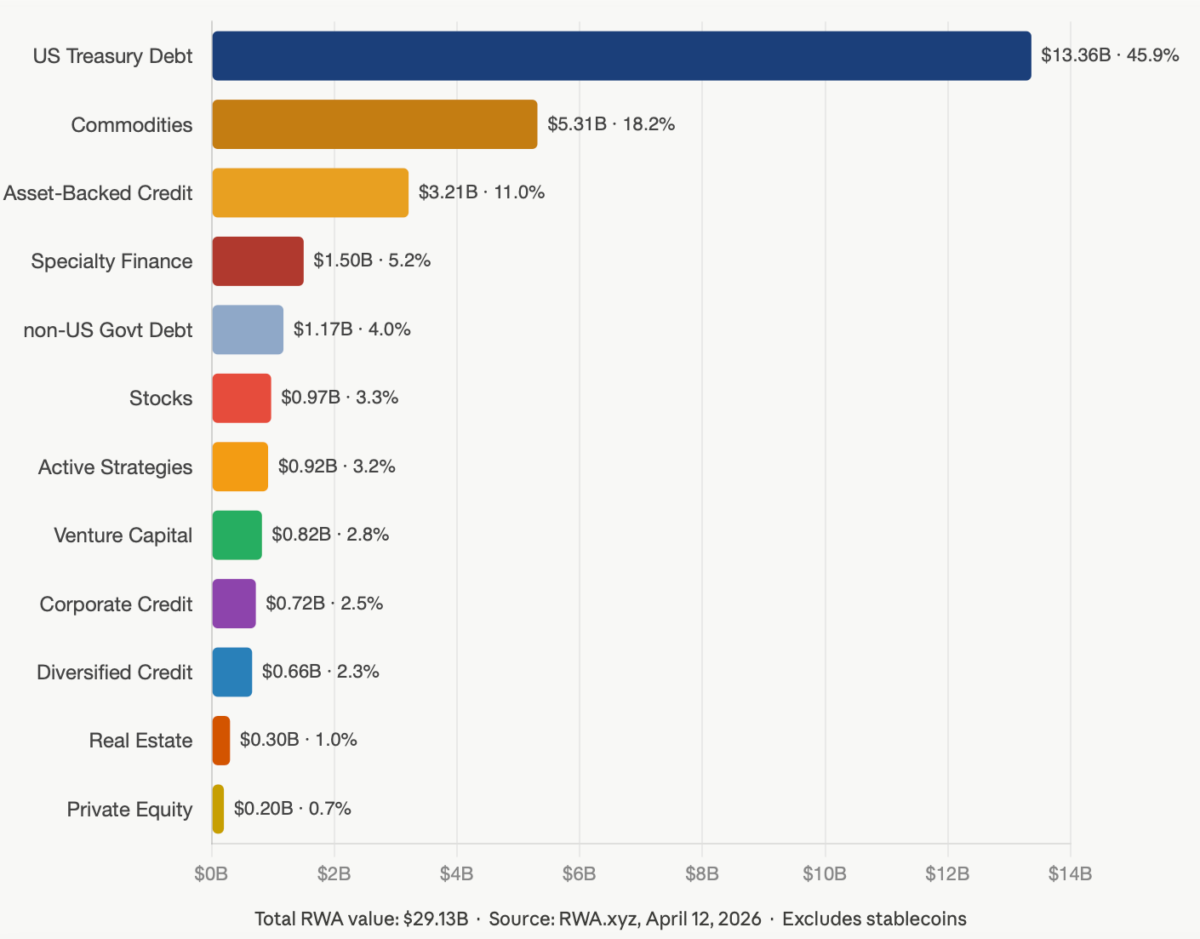

When you look at the split between asset classes, U.S. Treasuries dominate nearly half of the entire market. Commodities, led by tokenized gold, come next at over $5 billion, while asset-backed and private credit collectively contribute a meaningful share of the remaining volume.

This distribution is not accidental, it is a direct reflection of institutional participation. Capital is concentrating first in assets that are standardized, regulated, and yield-bearing. Tokenized Treasuries, in particular, mirror traditional money market demand, suggesting that institutions are not experimenting at the edges, but deploying capital into familiar instruments on new rails.

Beyond these assets, tokenized stocks have become the fastest growing category. In the past year alone, the tokenized stock market cap has grown from roughly $374 million to $982 million. In terms of total number of asset holders, this has skyrocketed from around 2000 to over 207,000 today.

The reason for this comes down to accessibility. Robinhood launched nearly 2,000 tokenized U.S. stocks and ETFs on Arbitrum. Many tier 1 centralized crypto exchanges like Coinbase, Kraken, Binance and Bybit launched tokenized stocks. The biggest players in TradFi have also taken note with the Nasdaq filing to list tokenized equities and the NYSE announcing a dedicated 24/7 tokenized securities platform.

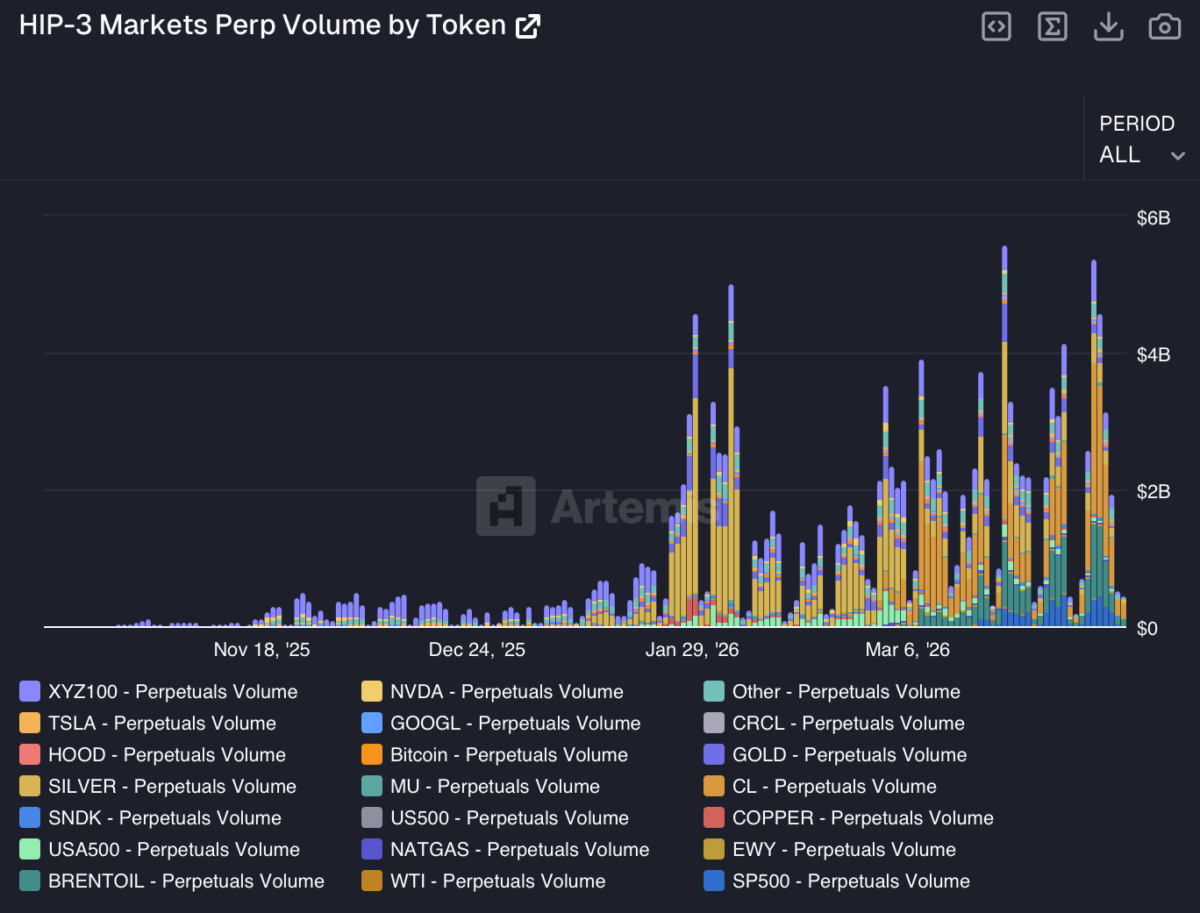

On the decentralized side, Hyperliquid’s permissionless HIP-3 framework has emerged as the infrastructure layer making this possible at speed, essentially allowing anyone to launch perpetual futures markets tied to equities and commodities without a gatekeeper. What’s striking is that the platform is now processing more commodities than even Bitcoin with WTI crude, Brent crude, Silver and Gold perps taking up the majority of the volumes.

Aster, backed by Binance’s investment arm YZi Labs and deeply integrated with the BNB Chain ecosystem, has emerged as one of the most credible challengers in this space, undercutting Hyperliquid on fees while leveraging Binance’s distribution network to scale rapidly.

Breaking Down the Numbers: What the Sentiment Reveals

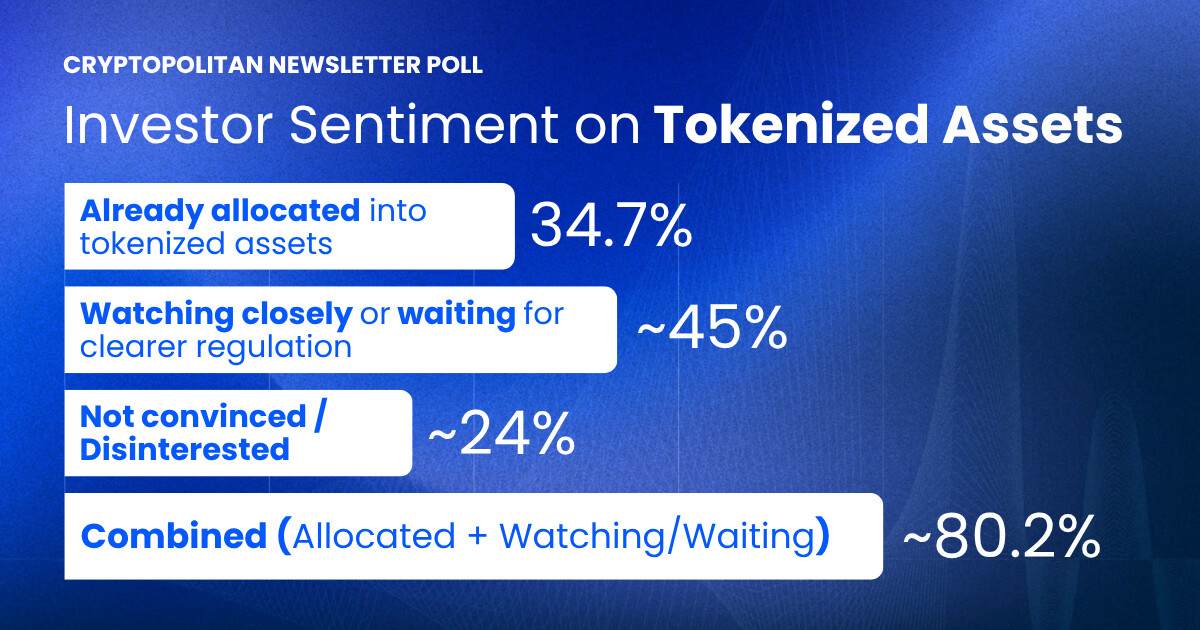

As done in Cryptopolitan’s previous report, the poll, conducted via the Cryptopolitan newsletter on April 6, 2026, provides a glimpse into how investors are viewing or positioning themselves in this market. The results reveal a clear pattern in that an audience who are investment aware across crypto, AI and tech is no longer dismissing tokenized assets but evaluating them and increasingly acting on that conviction.

34.7% of the respondents have already allocated into tokenized assets says a lot about adoption in the space. New narratives in the crypto space often fall under the trap of being overhyped with no real usage taking place under the hood. That said, when more than one in three participants are already using tokenized products, this shows that a large cohort have begun to move from awareness to execution.

At the same time, nearly half of the respondents are on the sidelines. They are waiting but not out of ignorance. The combined ~45% who are either watching closely or waiting for clearer regulation actually shows that a large group represents informed capital who understands the thesis but not yet compelled to act. Therefore, from a demand perspective, there is an audience looking to participate as soon as clearer frameworks come into effect. The final approval of the U.S. CLARITY Act could be the impetus that likely converts this cohort quickly.

The remaining around 24% are not convinced. This is perhaps the most revealing cohort. An audience that is digitally native, outright disinterest is less about rejecting tokenization and more about preference. Many could still be favouring direct crypto exposure or view RWAs as lacking the upside profile they seek.

All in all, the takeaway from the poll is that adoption right now is certainly uneven. That said, this kind of pattern is typical of early stage structural shifts that rarely stays uneven for long. The demand, however, is clearly there to see. With around 80.2% of respondents already invested in tokenized products or watching from the sidelines, this shows that an audience that tracks both traditional and emerging markets see this space as having crossed the credibility threshold into a serious portfolio consideration.

The smartest crypto minds already read our newsletter. Want in? Join them.

Read More