The post India Crypto Tax Alert: Section 148A Notices Target Unreported Trades appeared first on Coinpedia Fintech News

India’s tax authorities are now cracking down on crypto traders. The Income Tax Department has begun sending Section 148A notices for FY 2021–22, targeting unreported crypto transactions.

With exchanges, bank records, and PAN data under review, many traders could face reassessments and pressure to explain hidden profits.

Are you on their radar? Check it out!

Why Crypto Users Are Receiving India Crypto Tax Notices?

The notices are being triggered after the tax department began scanning trading data through its Insight Portal and risk engines. These systems compare PAN-linked KYC information, exchange transactions, bank movements, and ITR filings.

If mismatches appear, users may receive a Section 148A notice. This typically happens when crypto income was not reported, returns were not filed, or transaction trails appear incomplete due to multiple exchanges and wallets.

Many traders assumed reporting was not required in FY 2021–22 because crypto rules were unclear at the time. However, income disclosure was still mandatory, and authorities are now reviewing past activity.

Notices May Show Inflated “Undisclosed Income”

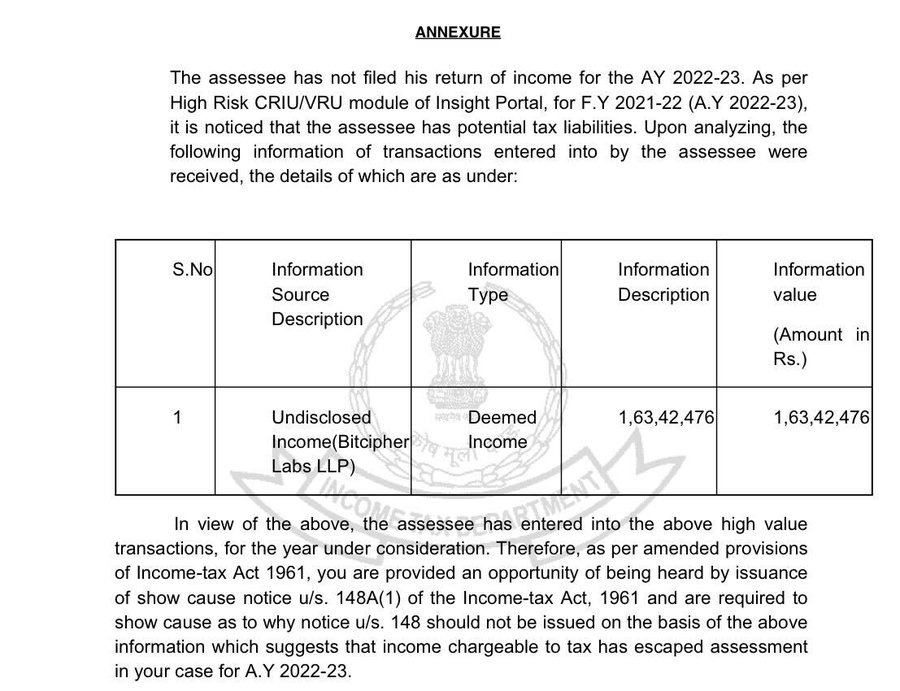

One major issue is that some notices display very high income figures. In certain cases, notices show amounts like ₹1.63 crore as “undisclosed income.” But this is often not the actual profit.

The system frequently calculates gross trading volume instead of net gains. For example, if a trader had a total trading volume of ₹ 1.6 crore but only ₹4–5 lakh in profit, the system may still flag the full ₹1.6 crore as income until it is clarified.

This usually happens when the tax department sees only partial transaction data.

Multiple Exchanges Increasing Risk

Users who traded across several platforms are more likely to get flagged. A typical flow, such as CoinSwitch to Binance, then to a wallet, and later to another exchange, can create gaps in the data.

If the system sees only deposits or withdrawals without the full chain, it may treat transfers as fresh income. This leads to inflated estimates and triggers notices.

Another major red flag is not filing an ITR for AY 2022–23 despite having crypto activity. In such cases, the risk score rises sharply.

Also Read : No Crypto Tax Cuts in India Budget 2026, New Penalties Introduced for Non-Compliance

148A Notice Is Not a Tax Demand

Importantly, a Section 148A notice is not a final tax demand. It is a show-cause notice asking the taxpayer to explain the mismatch before the assessment is reopened.

Recipients are advised to reconstruct all transactions, calculate actual gains or losses, and submit supporting documents. In many cases, proper reconciliation can resolve the issue.

The development signals that crypto transactions in India are now fully traceable through AIS data, exchange reporting, and KYC records.

With enforcement increasing, more notices for FY 2021–22 and FY 2022–23 are likely.

The post India Crypto Tax Alert: Section 148A Notices Target Unreported Trades appeared first on Coinpedia.org.

Read More