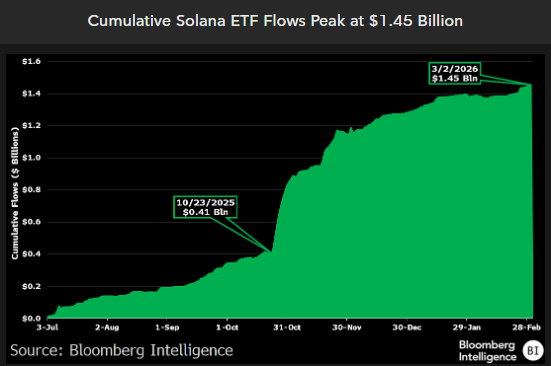

Spot Solana ETFs have pulled in roughly $1.45 billion since launching in July even as SOL fell 57% over the same stretch, a combination Bloomberg ETF analyst Eric Balchunas called “about as unlucky timing as you’ll ever see in ETFs.” For crypto markets, the takeaway is not just the headline flow number, but what it may say about the depth and quality of institutional demand.

Spot Solana ETFs Beat Bitcoin ETFs

Balchunas argued that the resilience of those inflows matters as much as their size. “Solana is down 57% since the spot ETFs launched in July … yet they managed to not only accumulate $1.5b in flows but not really give any of it up,” he wrote on X. He added that “50% of the assets are from 13F filers = serious inv base. Both really good signs for future IMO.”

The chart he shared shows cumulative Solana ETF flows climbing from about $410 million on Oct. 23, 2025, to $1.45 billion by March 2, 2026. The steepest acceleration came in late October through November, when cumulative inflows jumped sharply toward the $1 billion mark before continuing to grind higher into early March. Even with some flattening near the end of the period, the broader pattern is one of persistent net intake rather than hot-money churn.

Balchunas’ more provocative point was the relative comparison with Bitcoin. “The other thing about these flows, if we adjust for the size of solana vs bitcoin mkt cap, it’s the equiv of $54b in net new flows, which is about DOUBLE where bitcoin was at the same point,” he wrote. “And bitcoin was up a ton at that time vs down 57%. Anyhow, pretty impressive numbers given size and condition of the underlying mkt.”

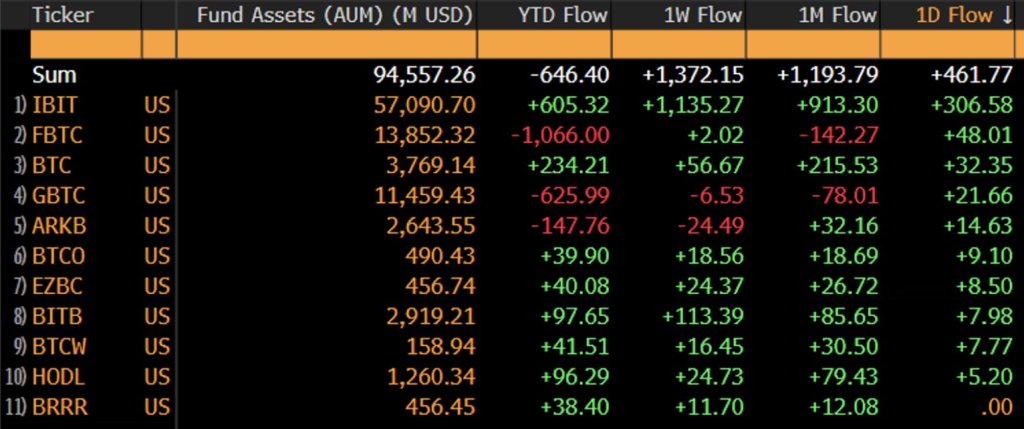

That comparison goes to the heart of the thesis. Absolute flows still heavily favor Bitcoin, whose US spot ETF complex sits near $94.6 billion in assets, according to the table Balchunas posted separately. BlackRock’s IBIT alone accounts for roughly $57.1 billion, while Fidelity’s FBTC and Grayscale’s GBTC hold about $13.9 billion and $11.5 billion, respectively. On Wednesday, the group took in another $461.77 million, with IBIT contributing $306.58 million.

But Balchunas used that same Bitcoin flow snapshot to make a broader point about the risks of drawing sweeping conclusions from short windows of market action. After noting that Bitcoin had risen 12% since the Iran strike while gold fell, he posed a deliberately overstated question: “So does that mean gold has failed as a safe haven and may be devoid of any purpose and vice-versa for btc?” He then answered it himself in the next post.

“I don’t actually think this btw, just trying to point out the problem with making these types of damning judgements of an asset based on a short term window of price action,” Balchunas wrote. “Gold has my respect as asset as does bitcoin. Bitcoin’s surge may have little to do w geopolitics but rather the Jane St bogeyman going away and vibe change. And ppl selling gold may just be taking profits, some may be looking for next run in btc, wth knows.”

The same logic applies to Solana. A 57% drawdown would usually be the sort of backdrop expected to choke off ETF demand, not sustain it. Instead, the Solana products appear to have attracted sticky capital and, at least in Balchunas’ framing, done so at a pace that compares favorably with Bitcoin once market-cap context is applied.

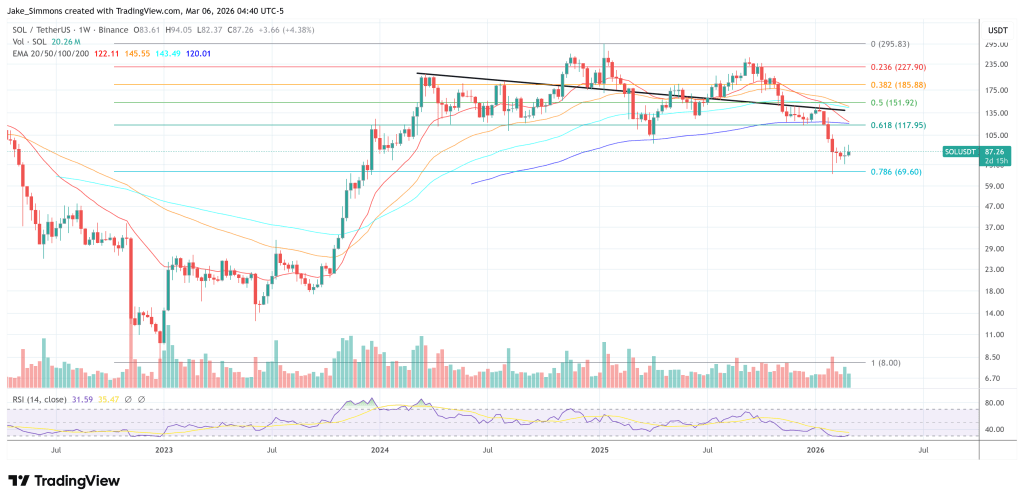

At press time, Solana traded at $87.26.

The post Solana ETFs Are Beating Bitcoin On Relative Flows Despite SOL Crash appeared first on Bitcoinist.

Read More